Mortgages: Categorising mortgage repayments as transfers (with the interest portion as an expense)

How a mortgage is set up and tracked in PocketSmith can vary from user to user! Check out our Overview guide for information on all our mortgage tracking methods, or continue reading to learn about our repayments as a transfer method 🏠⚡️

In this user guide

Overview

This method is great for

Fixed Mortgages

Floating mortgages

Offset mortgages

Revolving credit mortgages

Redraw facility mortgages

Note

If you are tracking your mortgage in PocketSmith, we also recommend adding your house as an asset to make your net worth more accurate. See Mortgages: Adding your home as an Asset

Categorising mortgage repayments as transfers (with the interest portion as an expense)

Reasons to set up a mortgage in this way

There are a few reasons that you may want to categorise your mortgage repayments as transfers:

- Accurate forecasting of net worth: If your home loan is included in PocketSmith as a loan account or home loan debt and your mortgage repayments are paid into the loan account or home loan debt, your overall net worth doesn't change. Therefore that movement of money from one account to another (eg. from an everyday account to a loan account) isn't seen as an expense, because what is debited from one account is then credited to another.

- Prevents double-counting your expenses, ie. the principal payment and the interest payment. The interest portion can be categorised as an expense to reflect the true cost

To accurately represent net worth, it's best to categorise the mortgage repayment into the loan account as a transfer and then treat the actual interest transactions that are automatically debited from the loan account as expenses—the interest transactions within the mortgage account are what cause a change in your net worth 📈 .

A good way to think about this is similar to how one might treat savings or investments - savings and mortgage payments are actually quite similar! With both of these, money is just being moved from one account to another, and the transfer of savings isn't really considered an expense ↔️ .

Category set up

In order to manage your mortgage within PocketSmith in this way, you'll need to create two unique categories, for example:

- Mortgage repayments (transfer)

- Mortgage interest (expense)

Note

If you have more than one mortgage account, you will need to create two categories for each of your mortgage accounts. For example;

- Home loan 1 Mortgage Repayments (transfer)

- Home Loan 1 Mortgage Interest (expense)

- Home Loan 2 Mortgage Repayments (transfer)

- Home Loan 2 Mortgage Interest (expense)

- Assign your mortgage repayments to your Mortgage repayments category, and ensure that this is set up as a transfer category.

- Assign both sides of the transfer to your Mortgage repayments category (for example, the transaction leaving one account, and then that same transaction entering another)

- Assign the interest transactions that are debited from your mortgage account to the Mortgage interest category. We recommend setting this up as a bill category.

Note

If you have your mortgage with ASB, your repayments will be split into two transactions for each side of the transfer - The interest portion and the principal portion. You will need to categorise all four of the transactions to the same transfer category

Budget set up

In order for your Net Worth forecast to be accurate, you'll need to set up the following budgets:

- A transfer budget for your Mortgage repayments category

-

An expense budget for your Mortgage interest category

-

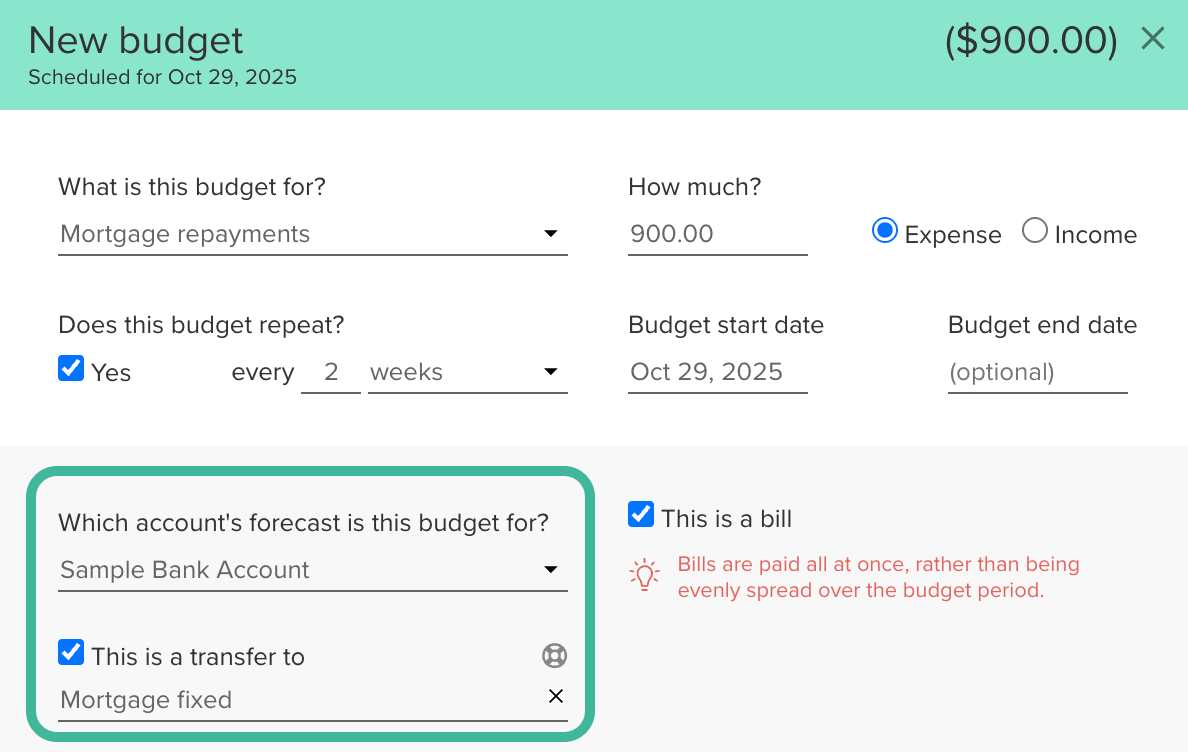

Create a transfer budget for your Mortgage repayments category.

This will allow you to track your transferred payments and allow PocketSmith to create an accurate forecast of your future account balances.

Under 'Which account's forecast is this budget for?' set the budget up so that it reflects a transfer from the account the repayments are made from to the mortgage account:

For the specifics of setting up a transfer budget see: Creating a transfer budget

-

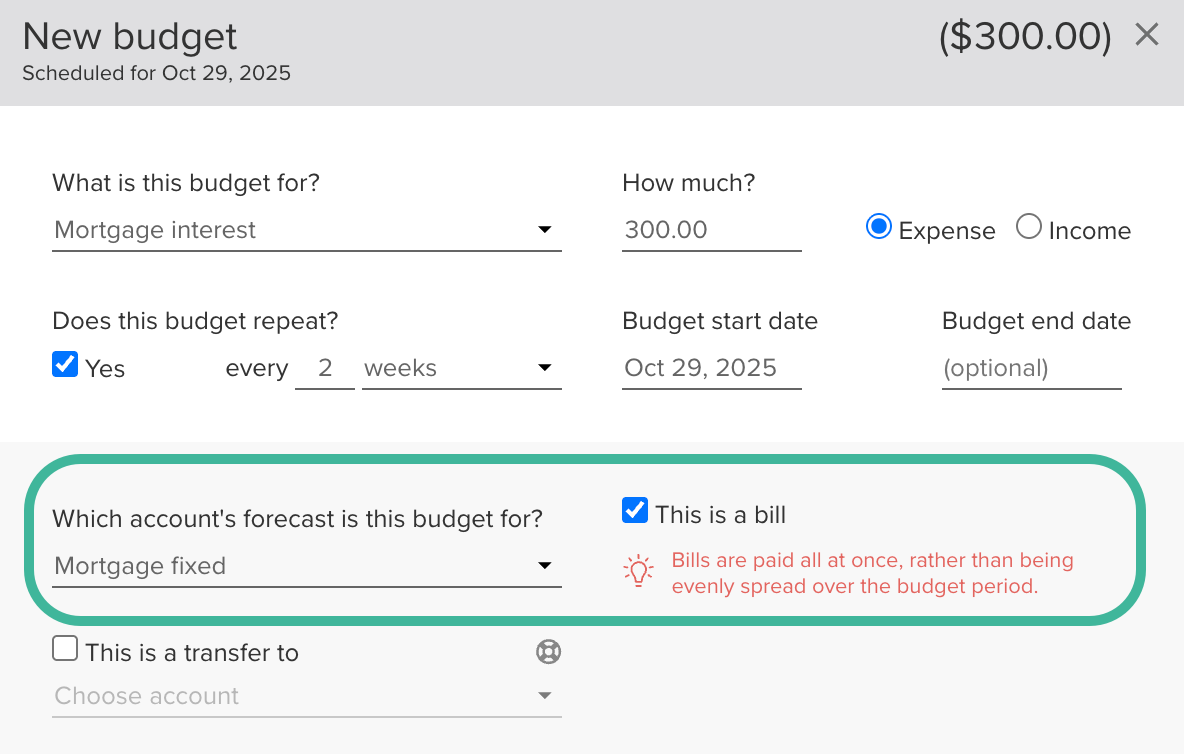

In order for your Interest payments to be reflected in your forecast, you'll also need to create an expense budget for your Mortgage Interest category.

- Under 'Which account's forecast is this budget for' select the account the interest is deducted from.

- Select This is a bill

Updating the expense interest budget periodically:

For the Mortgage Interest category, we recommend regularly updating the budget amount using the calendar page and selecting ' This and future budget events' option when applying any changes to more closely match the actual interest charged for your loan. This way, you can ensure that your forecast remains up-to-date and more accurate.

How this will affect your PocketSmith reports

By treating your principal Mortgage payments as a transfer, they will not be reflected on the Earning & Spending chart on the Dashboard nor in your overall spending budget at the top of the Budget page. Any Interest transactions will show as an expense.

Users can still create budgets for mortgage payments if they are set up as transfers so that they can be tracked! With a transfer budget set up, PocketSmith will automatically match the credit transaction to the debit transaction (or vice versa) for that budget, which will allow the user to keep track of their mortgage payments, and also allow PocketSmith to be able to create an accurate forecast of their future account balances. Check out our user guide: Creating a transfer budget.

Viewing repayments as an expense

To view your mortgage repayments as an expense, you can use the Income & Expense report (Reports > Income & Expense) instead of your Budget Summary.

When creating your Income & Expense report, ensure that you toggle Include transfers on so that they are included in the report. In addition, ensure that your mortgage accounts are not selected:

The expense side of the transfer budget, categorised under Mortgage Repayments, will then be shown as an expense in the report and included in the Total Expense.

Tip!

Doing this will show all your transfers for the selected accounts as expenses on the Income & Expense Statement; however, you can hide categories from the report to exclude other transfer categories.

It's a good idea to save the report so that it's easy to go back to. See: Saved Income & Expense reports for all the details.

Add your home as an Asset

Once you've added your mortgage accounts or home loans, don't forget to add your home or property as an Asset, as this will offset the loan in your Net Worth calculations 🏠 🙌

For details on adding your home as an Asset, see: Mortgages: Adding your home as an Asset

Managing property purchase and loan drawdown transactions

When first setting up your mortgage, you may need to categorise any initial transactions related to buying your home or property.

Mortgage drawdown transactions and initial property purchase transactions are best treated as transfers and categorised separately to avoid skewing your day-to-day spending or your loan repayment budgeting and reporting.

For all the details, check out: Mortgages: Property purchase and loan drawdown transactions